![]()

Investors seeking stable income and capital preservation often choose Guaranteed Investment Certificates (GICs) instead of market-based fixed income products such as bond funds, bond ETFs, or corporate bonds. GICs provide certainty and protection that many other fixed-income products cannot guarantee.

Fixed income investments typically provide predictable income but vary significantly in risk exposure, market volatility, and capital protection. Market-based fixed income products are traded securities whose prices fluctuate based on interest rate movements, issuer credit risk and market liquidity.

By contrast, GICs are deposit products issued by financial institutions that provide a guaranteed return if held to maturity, making them attractive to conservative investors and retirees seeking stability. They provide capital protection when held to maturity with 100% return of principal and interest.

This certainty becomes even more valuable during periods of heightened volatility or perceived valuation risk in equity markets. At the time of purchase, investors know the interest rate, the maturity date and the final value of the investment. GIC returns are not subject to market price fluctuations and maintain their value when held to maturity, even during periods when equities and bond prices decline. Consequently, GICs are typically used as part of a diversified fixed-income strategy, rather than as a substitute.

These characteristics provide portfolio stability and precise liquidity planning through structured strategies such as GIC laddering which eliminates the risk of forced liquidation of volatile assets. GIC laddering is a portfolio strategy in which an investment is spread across multiple GICs with different maturity dates, rather than investing all funds in a single term. The goal is to balance interest rate risk with improved liquidity and stability of return.

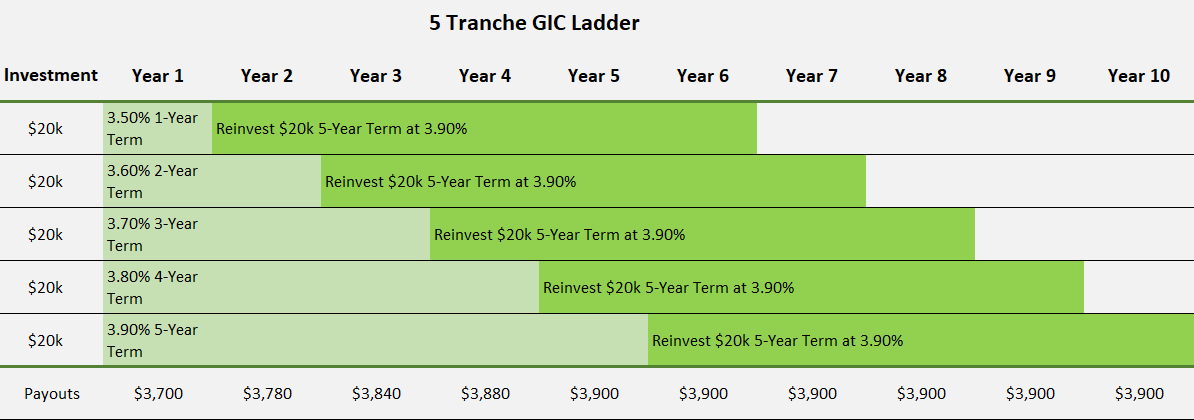

A GIC ladder can produce a predictable annual income. Our example assumes that an investor has $100,000 to invest, and that 5-year GICs typically offer higher returns in a normal upward-sloping yield curve environment. Instead of investing $100,000 in one 5-year GIC, the investment is divided into 5 equal tranches of $20,000. To construct a 5-year GIC ladder the investor, ideally with the assistance of a Deposit Broker, invests $20,000 in each of 1, 2, 3, 4, and 5-year GICs.

After a year, the 1-year GIC matures and the proceeds are reinvested in a new 5-year GIC. Each year, one GIC matures and is reinvested in a 5-year GIC. Over time, the portfolio becomes a rolling ladder of 5-year GICs, with one maturing every year. If rates rise the maturing GICs can be reinvested at higher rates. If rates fall the existing longer-term GICs preserve higher locked-in rates. This reduces the impact of interest rate cycles.

The ladder ensures predictable annual income. Access to annual maturity proceeds reduces the need to break non-redeemable GICs early, which may be restricted or subject to penalties. This is especially useful for retirement Income planning, aligning maturities with annual withdrawal needs, reducing the effects of market volatility, capital preservation mandates, and ensuring ongoing access to insured, low-risk funds.

A primary benefit of investing in GICs is that Deposit Brokers ensure that the recommended GICs are protected by government-backed insurance through the Canada Deposit Insurance Corporation (CDIC) or a provincial guarantor such as the Financial Services Regulatory Authority of Ontario (FSRA) and the Deposit Guarantee Corporation of Manitoba (DGCM). Descriptions of federal and provincial deposit insurance in Canada can be found in the chart on the Registered Deposit Brokers Association website www.rdba.ca in the drop-down menu under GIC Investors.

CDIC insures eligible deposits up to $100,000 per depositor, per category, per institution, in Canadian dollars, regardless of term or currency. Some provincial guarantors offer higher or unlimited guarantees. Most other fixed-income products do not offer comparable protection.

In summary, GICs are straightforward investments that do not require an understanding of duration, credit spreads, or Net Asset Value (NAV) volatility. They are simple to implement and manage particularly with the support of trained Deposit Brokers. They are widely used as a core conservative investment in Canada. In periods of market uncertainty, GICs provide not only safety, but also strategic flexibility and behavioral discipline, making them an essential component of prudent portfolio construction.

To learn more about GICs and the advantages of working with a knowledgeable Deposit Broker visit www.rdba.ca. Try our interactive RDBA Broker Advantage Index, which is a graphical representation of the advantages of working with an RDBA Deposit Broker. Use our Find a Broker search engine to connect with a screened, trained and tested professional RDBA Deposit Broker.

![]()